Notes to the Financial Statements 19-35

Note 19 Debtors Note 20 Creditors: amounts falling due within one year Note 21 Creditors: amounts falling due after more than one year Note 22 Deferred capital grant Note 23 Recycled capital grant fund

Note 24 Community benefit fund Note 25 Loans and borrowings Note 26 Financial instruments Note 27 Pensions Note 28 Non-equity share capital

Note 29 Cash flow from operating activities

Note 30 Net debt reconciliation

Note 31 Capital commitments

Note 32 Operating leases

Note 33 Contingent assets/liabilities

Note 34 Related parties

Note 35 Post balance sheet events

19 Debtors

Social housing rental arrears were 2.77% at the end of the year (2022: 2.25%).

20 Creditors: amounts falling due within one year

21 Creditors: amounts falling due after more than one year

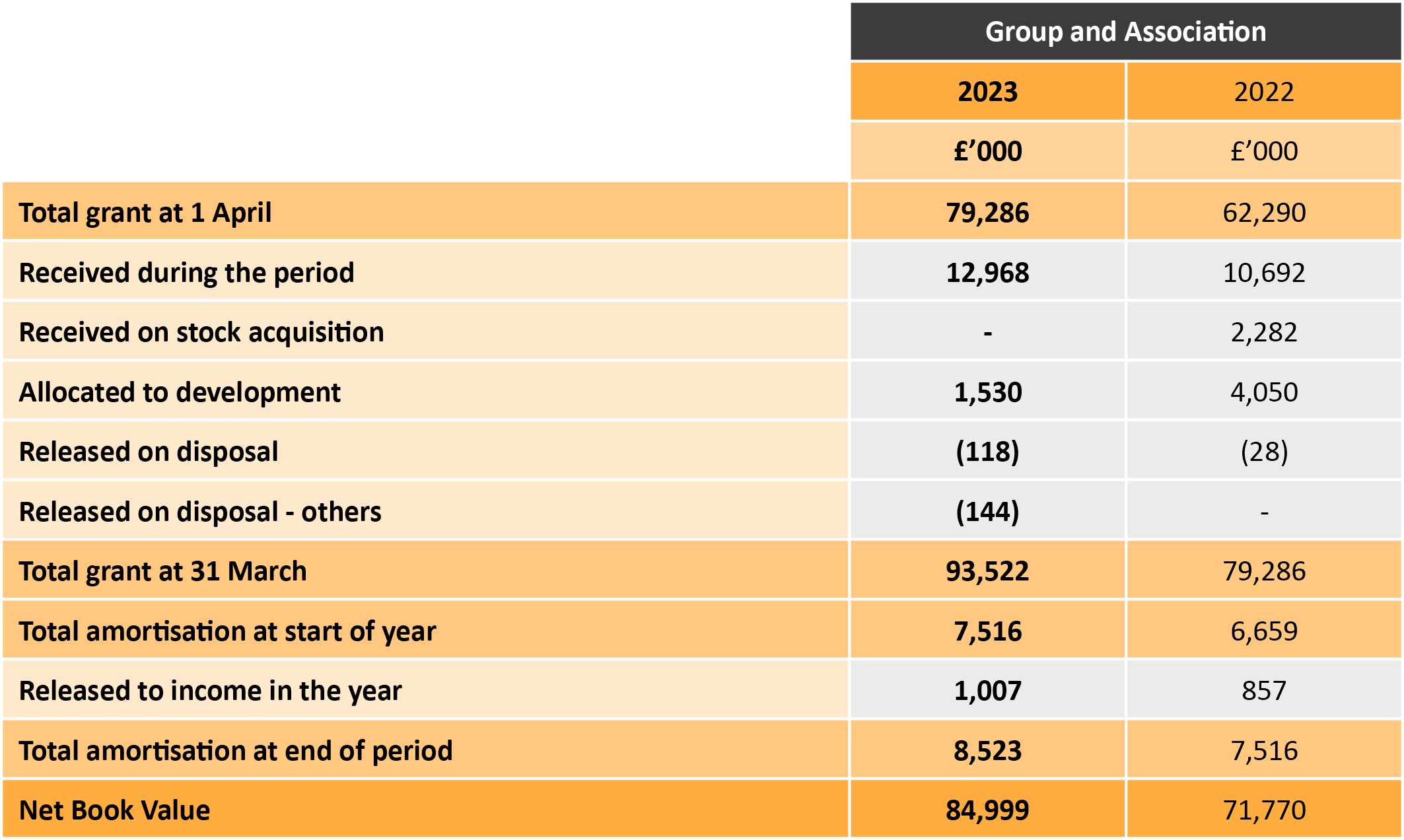

22 Deferred capital grant

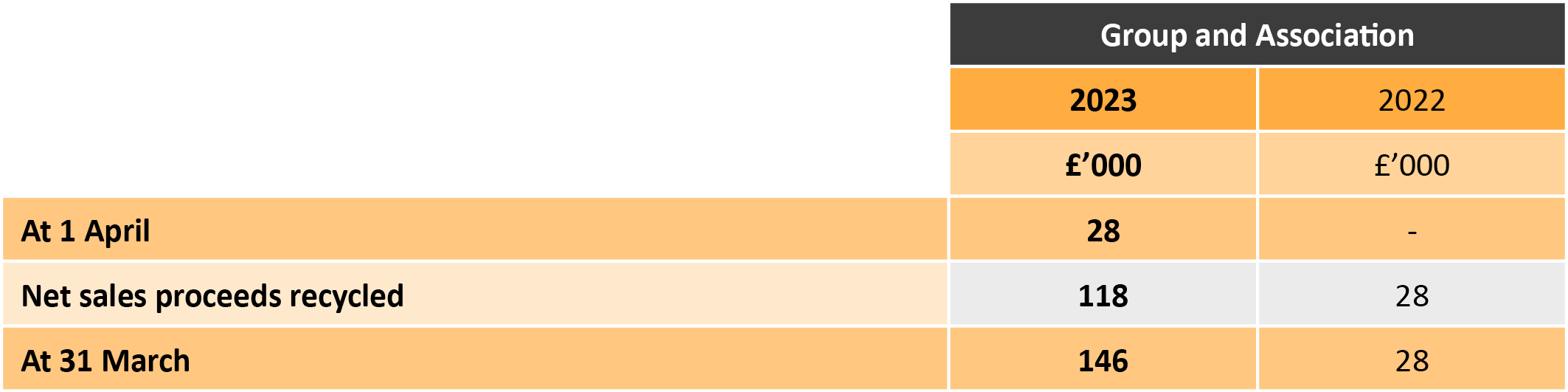

23 Recycled capital grant fund

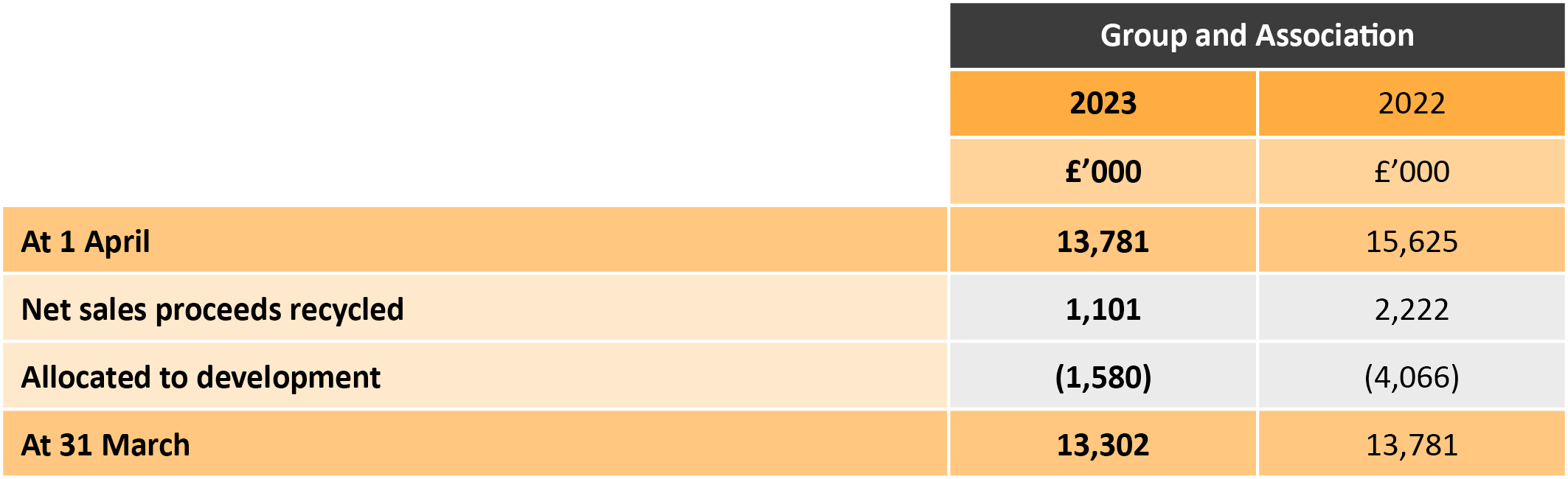

24 Community benefit fund

In 2003, settle was the recipient of a Large-Scale Voluntary Transfer (LSVT) of housing properties from North Hertfordshire County Council. In exchange for receiving so many homes at significant discount, settle agreed to restrict income from any subsequent sales to a predefined low value until 2030. The remaining proceeds from each sale are recognised here as a creditor, repayable on demand.

The signed agreement states that these funds can only be spent on developing new social housing or associated community facilities within the local area.

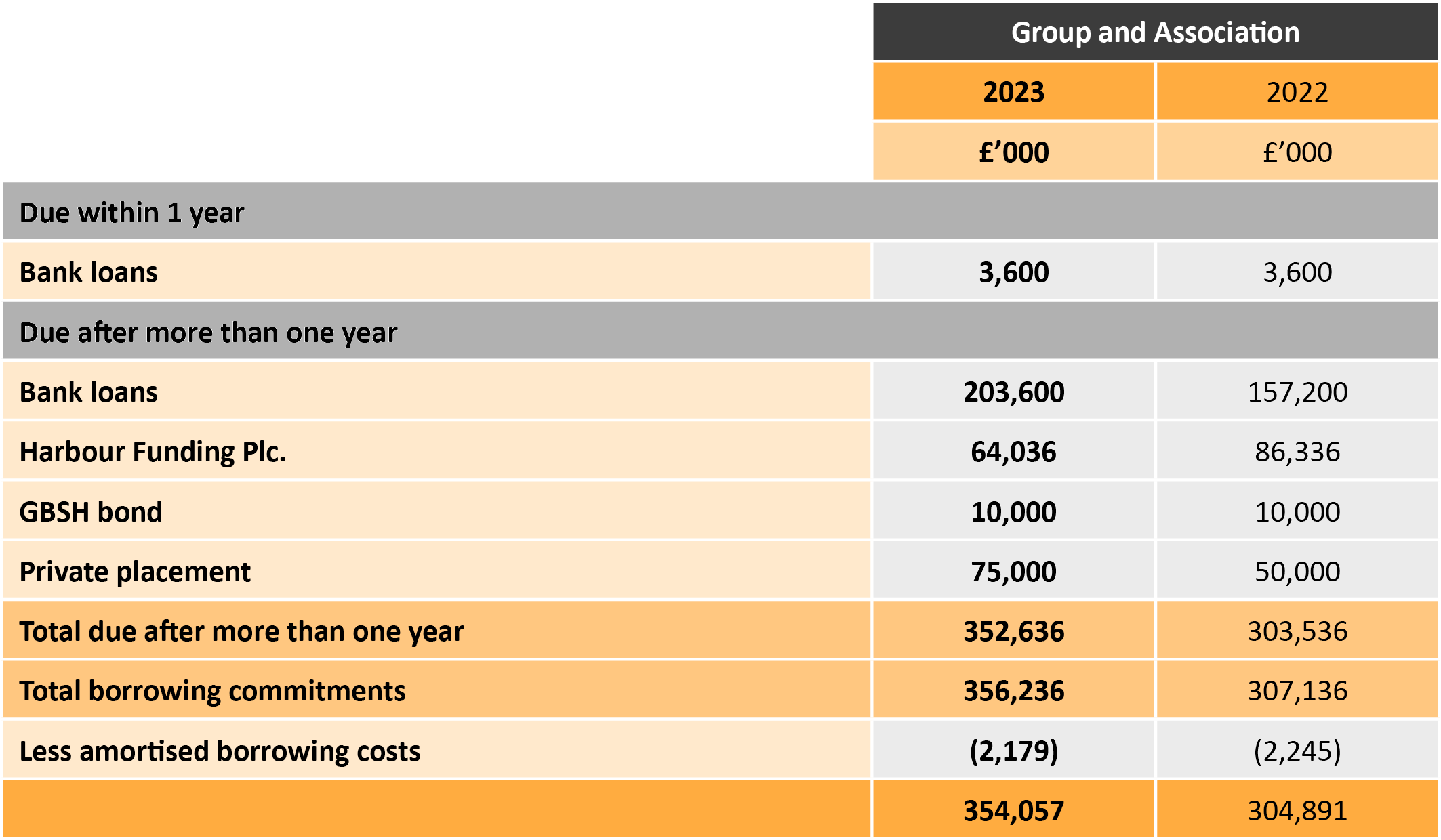

25 Loans and borrowings

Debt analysis

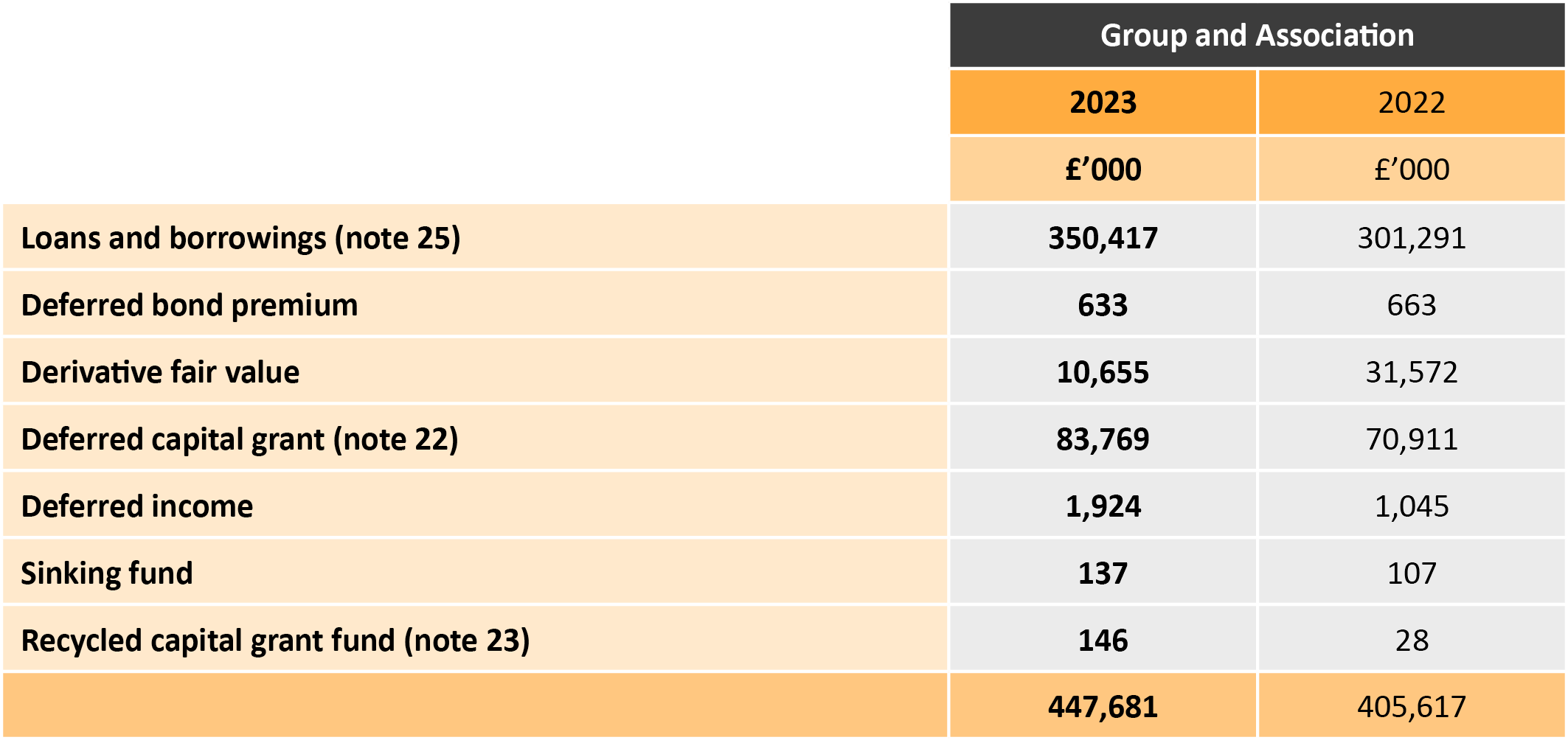

Security

All borrowing is secured by fixed charges on individual properties.

Terms of repayment and interest rates

At 31 March 2023 the Group had undrawn loan facilities of £143m (2022: £143m).

The Group interest rate for the loans and borrowings are as follows:

- Bank loans are under four term loans of £75.6m, £54.6m, £27m and £50m at floating rate of SONIA+0.69%, SONIA+0.71%, SONIA+1.15% and SONIA+1.02% respectively;

- Harbour Funding Plc borrowing is at a fixed rate of 5.28%;

- GBSH bond is at a fixed rate of 5.19%; and

- Private placement borrowing is under three term loans of £20m, £30m and £25m at a fixed interest rate of 2.3%, 2.33% and 2.37% respectively.

- The Group has entered into floating to fixed interest rate swaps with the fixed leg of 4.80%, 4.57% and 3.97% and the variable rate leg equal to SONIA plus margin. These has been accounted for under hedge accounting (see note 26).

Based on the lender’s earliest repayment date, borrowings are repayable as follows:

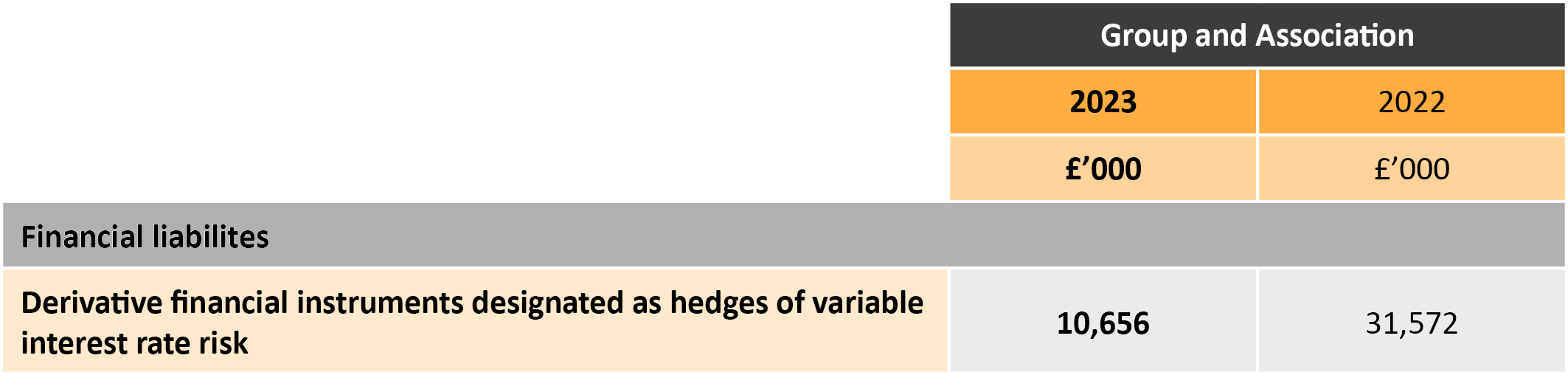

26 Financial instruments

Information regarding the Group’s exposure to and management of credit risk, liquidity risk, market risk, cash flow interest rate risk, and foreign exchange risk is included in our Treasury Management Policy.

The carrying values of the Group and Association’s financial liabilities measured at fair value through Statement of Comprehensive Income are summarised by category below:

Derivative financial instruments designated as hedges of variable interest rate risk comprise interest rate swaps.

Hedge of variable interest rate risk arising from bank loan liabilities

To hedge the potential volatility in future interest cash flows arising from movements in SONIA, the group has entered into floating to fixed interest rate swaps with a nominal value equal to that initial borrowings, the same term as the loans and interest re-pricing dates identical to those of the variable rate loans. These result in the group paying a fixed rate and receiving SONIA (though cash flows are settled on a net basis) and effectively fix the total interest cost on loans.

The derivatives are accounted for as a hedge of variable rate interest rate risks, in accordance with FRS 102 and had a fair value of £10.6M (2022: £31.6M) at the balance sheet date. The cash flows arising from the interest rate swaps will continue until their maturity. The change in fair value in the period was £20.9m; £3.3m charge as movement in fair value of financial instruments in the statement of comprehensive income and £17.6m the financial instrument hedging reserves.

The Group has applied the Amendments to FRS 102: Interest rate benchmark reform (Phase1 and Phase 2).The Group has taken advantage of these amendments in relation to the SONIA interest rate noted above.

27 Pensions

settle Group Stakeholder Pension Scheme (SPS)

The SPS pension scheme is defined contribution pension scheme administered by Legal & General. It is the current pension scheme offered to new employees in the company. The employer’s contributions to SPS by the Group for the year ended 31 March 2023 were £1,525k (2022: £704k).

Local Government Pension Scheme (LGPS)

The LGPS is a multi-employer scheme, administered by Hertfordshire County Council Pension Fund under the regulations governing the LGPS, a defined benefit scheme. The most recent formal actuarial valuation was completed as at 31 March 2020 by a qualified independent actuary.

The LGPS is closed to employees who join the Group after 31 March 2003. The liability in respect of past service for transferring members as at 31 March 2003 is to remain with North Hertfordshire Council (NHC). The market value of the scheme's assets as at 31 March 2003, and any deficit or surplus relating to revaluation of these assets, are reflected in the financial statements of NHC.

The employer's contributions to the LGPS by the Group for the year ended 31 March 2023 were £128k (2022: £278k) at a contribution rate of 21.2% of pensionable salaries.

During the period between pension valuation and publication of these financial statements, new guidelines were issued for pension liability recognition, following a December 2018 tribunal appeal which overturned a previous ruling relating to age related entitlements. The impact of the case has now been implicitly built into the new actuarial valuation of the fund for the three-year period starting 1 April 2020.

Principal actuarial assumptions: Financial assumptions

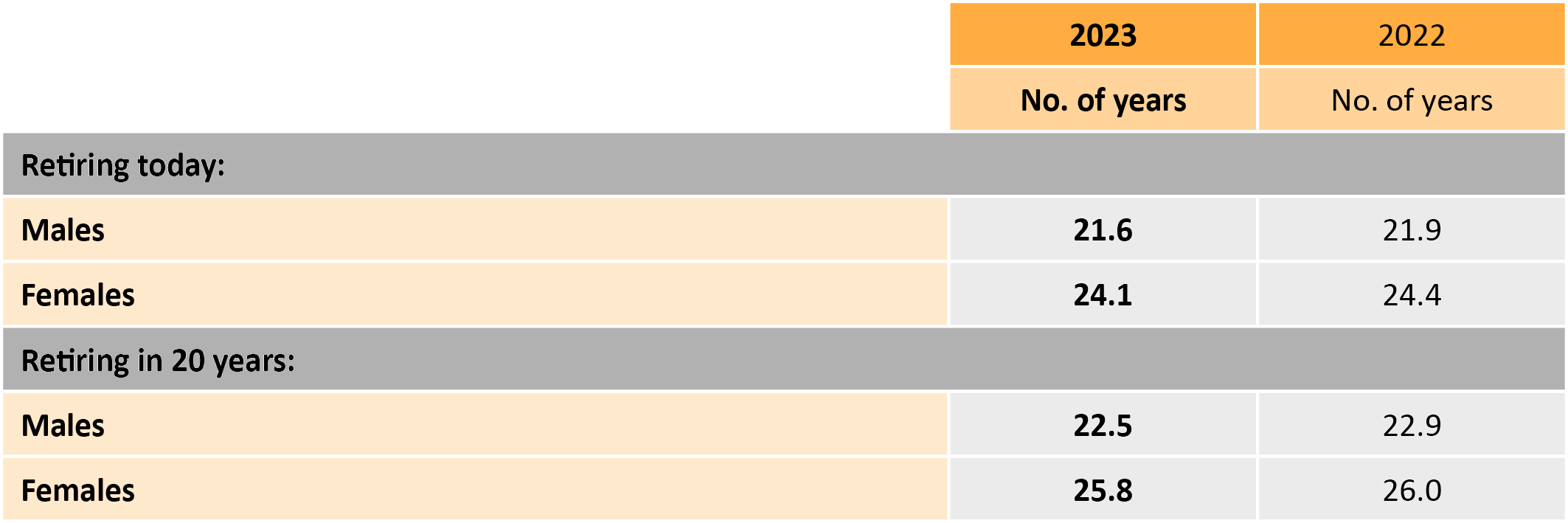

Mortality assumptions

The post-retirement mortality assumptions adopted to value the benefit obligation at March 2023 and March 2022 are based on the CMI 2021 with a 10% weighting of 2021 (and 2020) data, smoothing (Sk7), initial adjustment of 0.25% and a long-term rate of 1.5% p.a. for both females and males. This assumption has changed from last year (a 10% weighting parameter has been applied) to approximately reflect the higher than expected observed deaths in 2022.

The assumed life expectations on retirement at age 65 are:

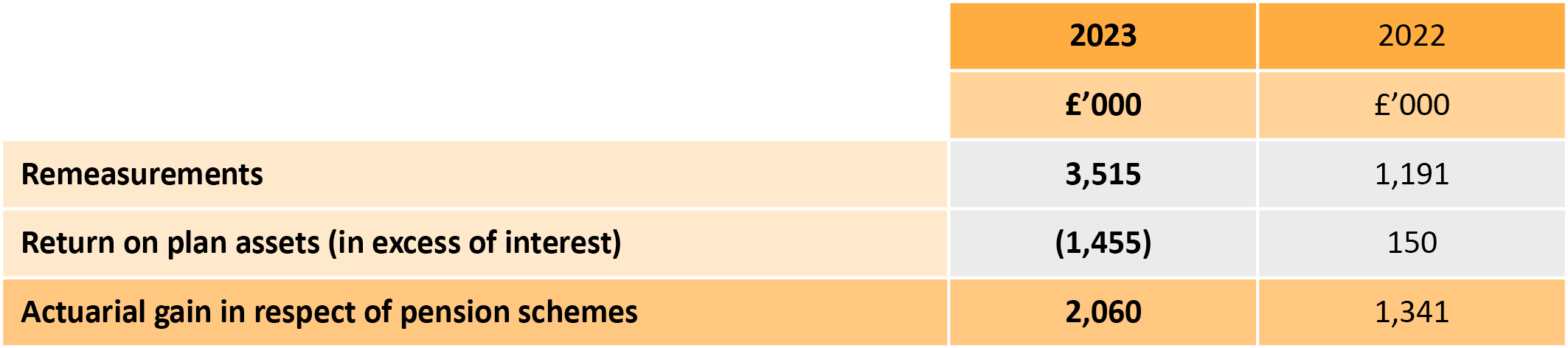

Amounts recognised in surplus or deficit

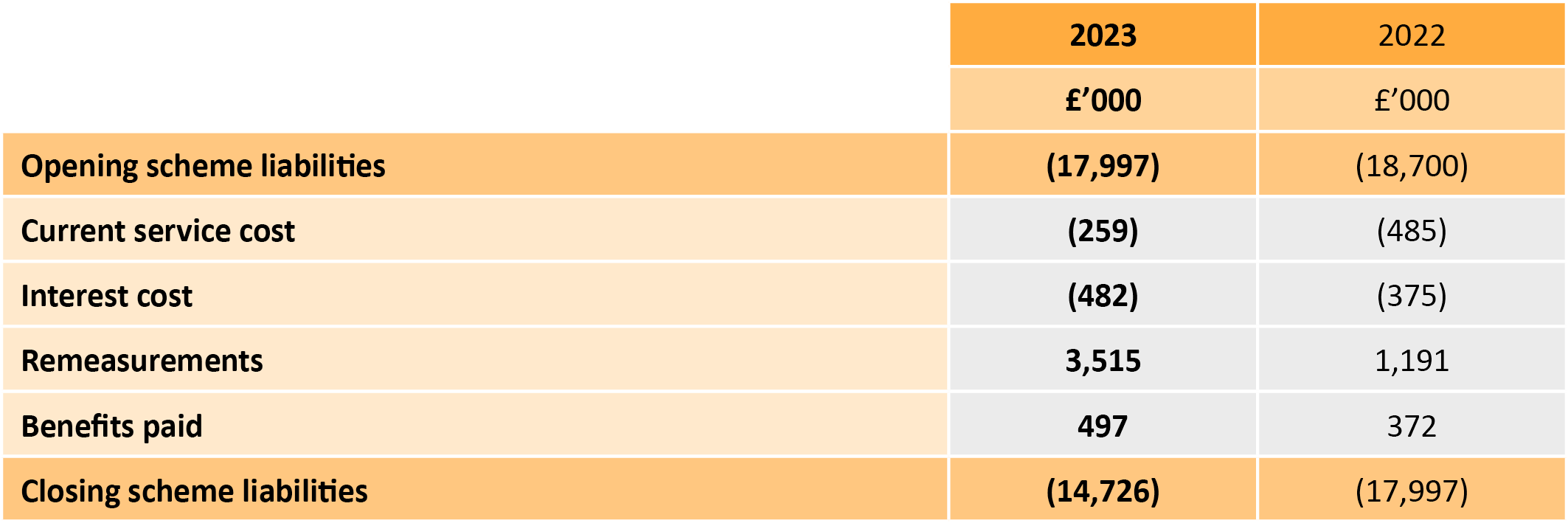

Reconciliation of opening and closing balances of the present value scheme liabilities:

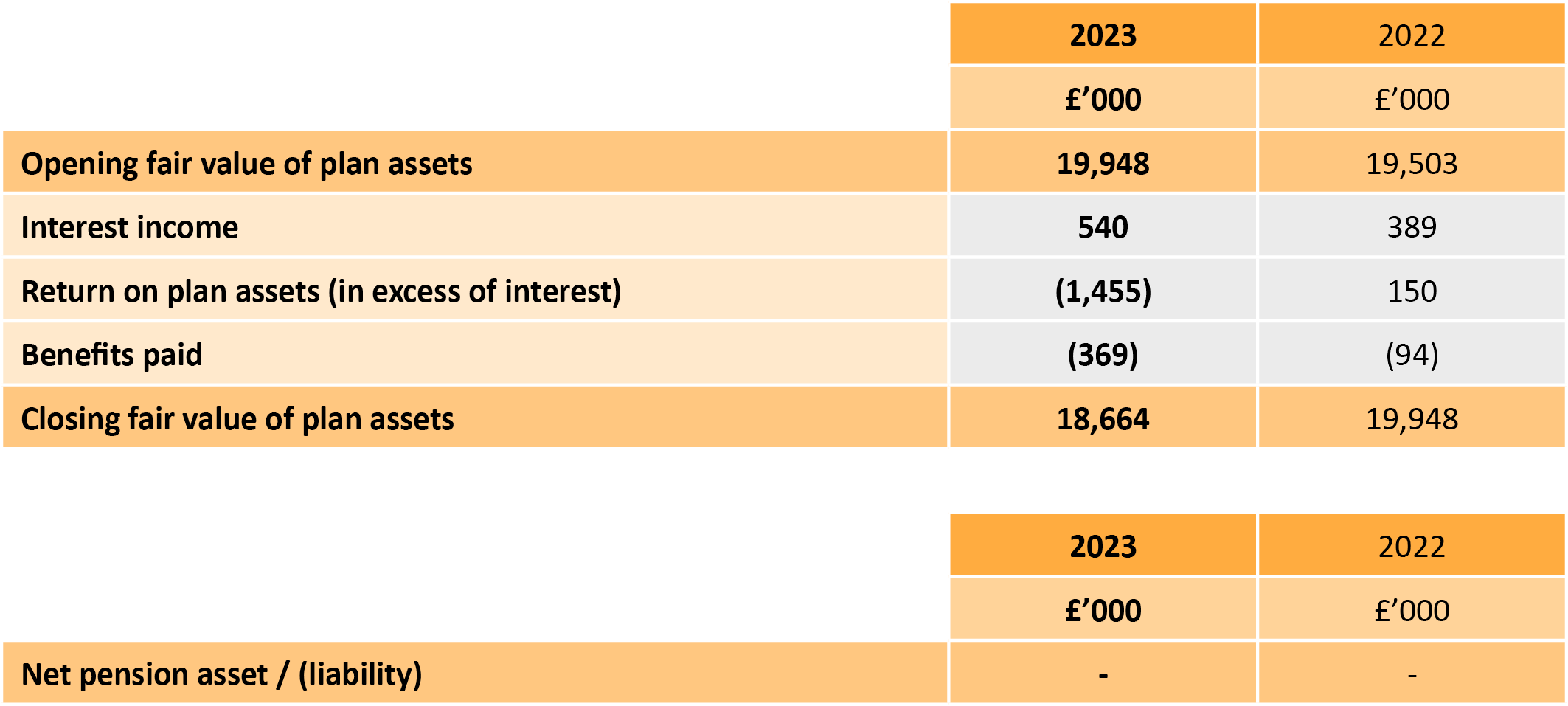

Reconciliation of opening and closing balances of the fair value of plan assets:

While the calculations above would leave settle in a surplus position of £3.938m (2022: £1,951m), LGPS cannot demonstrate that the Association could take advantage of the asset position in reduced payments or take ownership upon death of the final living scheme member. As a direct result, settle cannot recognise the surplus as LGPS does not form a debtor to the Association. The pensions liability is therefore capped at nil, leaving a total movement in reserves of £73k, comprised of the recognisable portion of the remeasurements.

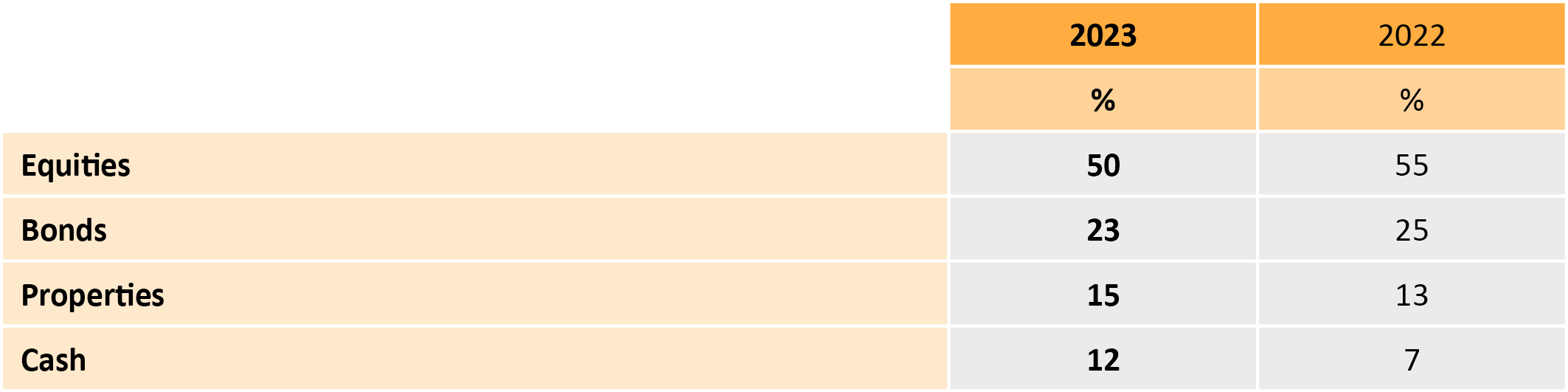

Major categories of plan assets as a percentage of total plan assets:

28 Non-equity share capital

The shares provide the members with the right to vote at the General Meeting, but do not provide any rights to dividends or distributions on a winding up.

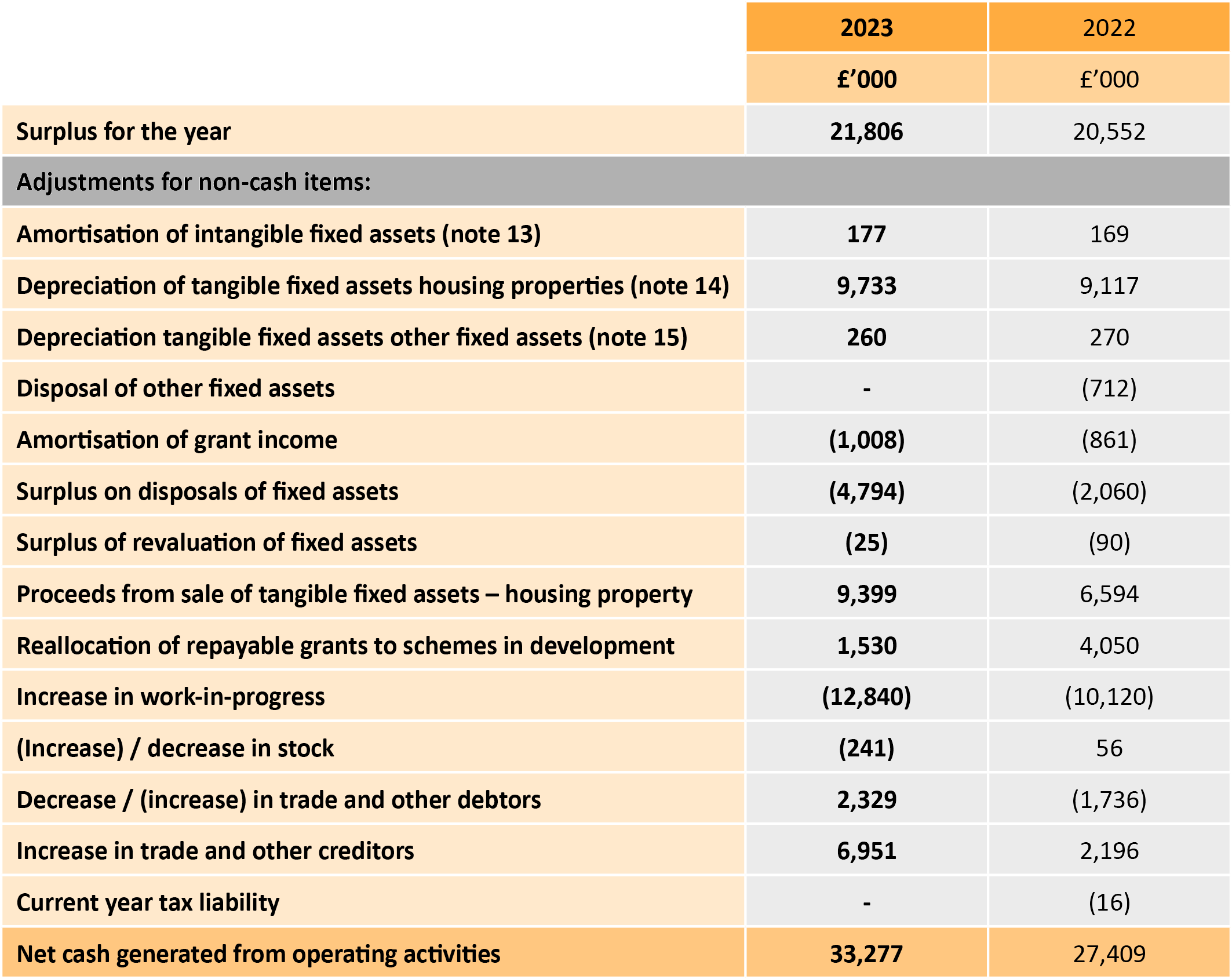

29 Cash flow from operating activities

30 Net debt reconciliation

31 Capital commitments

The above commitments will be financed primarily through a mixture of operating cashflows, borrowings and any Social Housing Grant obtained in the year.

32 Operating leases

The Group has not entered any operating leases (2022: none).

33 Contingent assets/liabilities

There are no contingent assets or liabilities as at March 2023.

34 Related parties

Related party disclosures

The ultimate controlling party of the group is settle Group – Registered social housing provider. There is no ultimate controlling party of settle Group.

Subsidiary and associated companies

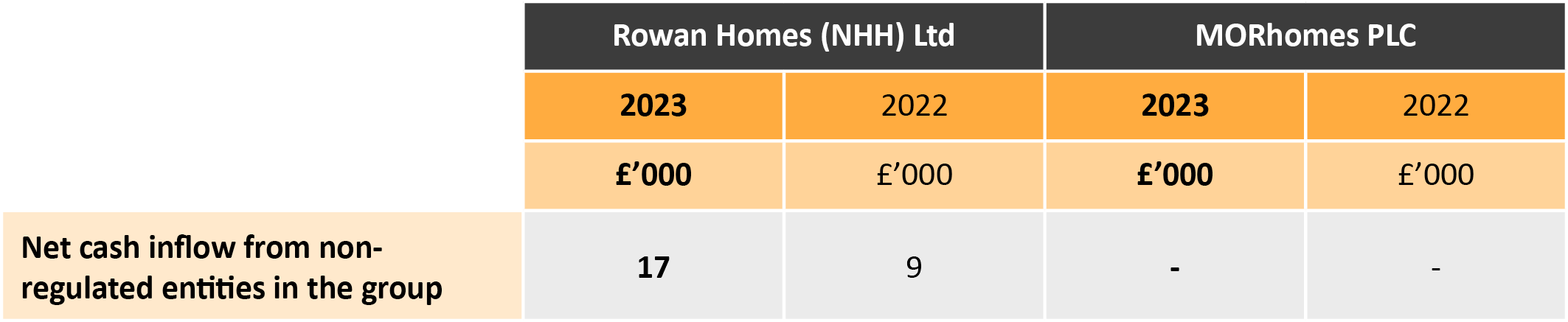

settle has no regulated subsidiary or associated undertakings. The following transactions that took place between the Group and its non-regulated associated companies during the year were:

Development costs are allocated on actual amount incurred on accrual basis.

Intercompany balances at the end of the year were as follows:

The intercompany balance due from the subsidiary undertaking is repayable on demand.

During the year no compensation (2022: nil) was paid to key management personnel for loss of office.

One of the current Board members is a Key Management Personnel of HACT, a charity that supplied goods and services totalling £17,880 (2022: £11,400) to settle Group during the year.

35 Post balance sheet events

There are no post balance sheet events.